Onit is a digital-first bank helping SMEs and individuals manage money, receive payments, and access financing without traditional banking friction.

Mobile web

Role

Product designer

Deliverables

User research and synthesis, Ecosystem mapping, User flows and information architecture, Core banking experiences, KYC and onboarding flows, Payments and transfers, Credit and financing experiences, Design system development, Prototype testing and validation

Product managers, Engineers, Operations teams, and another designer to design the foundation of Onit's banking experience.

Scope

Workflow redesign, information architecture, system patterns, UI components

THE OPPORTUNITY

Traditional banks impose lengthy onboarding processes and fees. Mobile money services simplify payments but become expensive for businesses operating at scale.

As Onit evolved from a lending platform into a licensed digital bank, we saw an opportunity to create a banking experience that was transparent, affordable, and designed around how businesses actually operate.

Goals

What we were up against

MSMEs in Kenya, ~40% of GDP

Of Kenya's mobile money market is M-Pesa

Financially included, vs 27% in 2007

Time to open an Onit account

Sources: KNBS 2024 FinAccess survey, Communications Authority of Kenya 2024–25, Onit product data. Note: Kenya is already ~85% financially included via mobile money, so "unbanked" undersells it. The real gap is formal banking and SME-specific tools, worth a phrase tweak in your copy.

RESEARCH

Understanding the financial ecosystem

Before designing solutions, we needed to understand how money moved through the SME ecosystem, not how it moved through a bank.

10k+

SMEs Studied

40+

Interviews

1000+

Surveys

Cross team

Workshops with product, ops, compliance

Key Insights

Three patterns came out of the interviews and workshops. Each one sets up one of the challenges ahead.

Synthesizing insights from interviews, surveys, and stakeholder workshops.

CHALLENGE 1

Building trust in a free bank

One of the most surprising findings from research was that users did not trust free banking.

People assumed hidden fees would eventually appear.

The challenge wasn't communicating value.

The challenge was making value visible.

Userflows

Initial explorations

CHALLENGE 2

Reducing KYC Friction

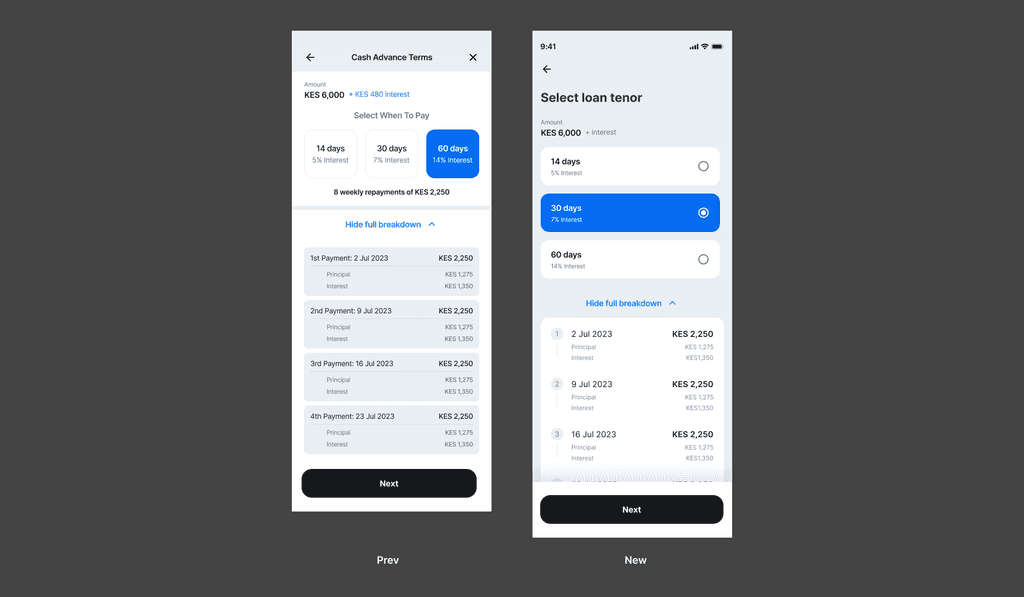

Regulations required identity verification. Users wanted immediate access. The business needed activation. We weighed three approaches and chose progressive verification.

Final KYC Screens

CHALLENGE 3

Designing banking around business growth

SMEs didn't need another bank account. They needed tools to run the business. That shifted our focus from transactions to outcomes

BUILDING FOR SCALE

A system that kept design and engineering in sync

As the product matured, consistency mattered more than novelty. A shared component library accelerated delivery and closed the gap between design and engineering.

Iterative Testing and Collaborative Development

Every major experience was tested before build. Feedback shaped onboarding, payments, and account management across multiple rounds.

Trust can be designed

Deliver value before asking for commitment.

Trust is earned through product experience, not messaging.

Banking products should support growth, not just transactions.